Last week was a big one for monetary policy and economic data. The Federal Reserve raised interest rates 0.75%, with unanimous agreement that higher rates were required to bring inflation under control. In his press conference, Fed Chair Jerome Powell announced the Fed was becoming more data dependent. The market interpreted that statement to mean rate hikes would likely slow in the future, especially if inflation starts moving lower.

Key Points for the Week

- The Federal Reserve raised rates 0.75% to a range of 2.25-2.50%.

- U.S. gross domestic product declined 0.9%, restrained by falling goods purchases and slower inventory growth.

- The S&P 500 gained 9.2% in July, its best month since COVID vaccine data was released in November 2020.

U.S. GDP shrank for the second consecutive quarter, contracting by 0.9%. Much of the economy remains strong, and services consumption continues to increase. Weakness in goods, inventories, housing, and government spending are contributing to signs the economy is slowing.

The Personal Consumption Expenditures (PCE) Price Index confirmed the earlier Consumer Price Index report that inflation remains a challenge. PCE was up 1.0% as fuel prices added to pricing pressure in other sectors. Core PCE, which excludes food and energy, rose 0.6%.

Markets welcomed the idea the Fed may slow interest rate hikes sooner than expected. The S&P 500 gained 4.3% last week to complete a 9.2% rally for the month. The global MSCI ACWI rebounded 3.3%. The Bloomberg Aggregate Bond Index jumped 0.6%.

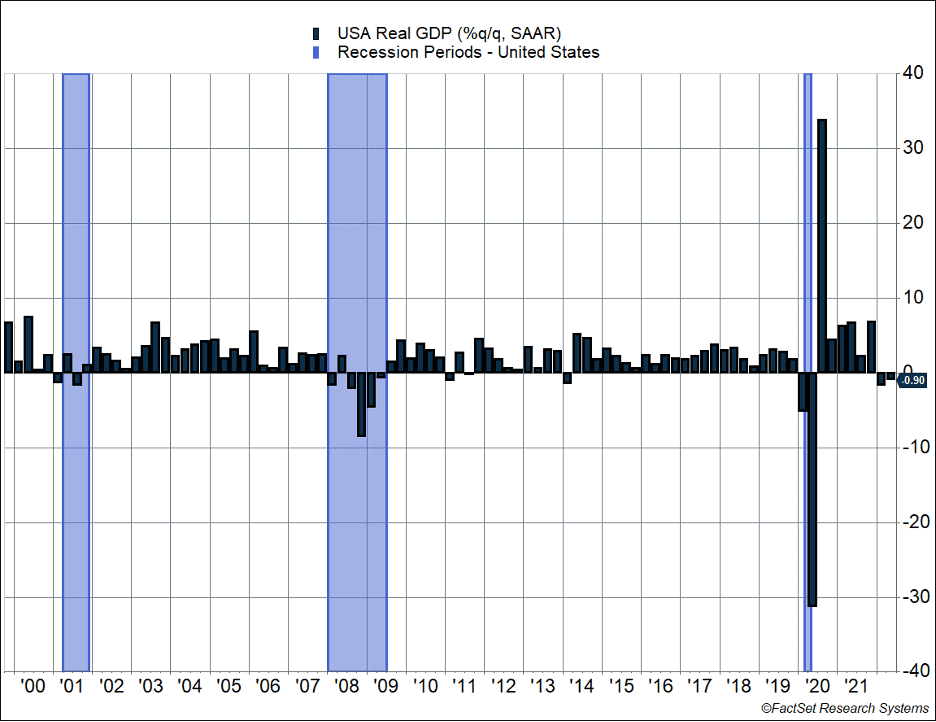

Figure 1

Are We in a Recession?

Many investors seem to have learned that two quarters of declining GDP means the country is in a recession. Yet, this definition isn’t totally accurate. There are far more factors the National Bureau of Economic Research (NBER) uses to determine whether there is a recession, but for much of the public, the two-negative-quarters definition seems to have stuck.

Like most rules, two quarters of economic decline isn’t a terrible test for a recession. The NBER defines recession as, “…a significant decline in economic activity that is spread across the economy and lasts for more than a few months.” Two quarters of declining GDP is usually significant, affects the broad economy, and lasts for more than a few months.

Reality indicates recessions are more complicated. Figure 1 shows none of the last three recessions matches the popular definition of two consecutive quarters of GDP growth. The 2001 recession had two nonconsecutive quarters of growth. The Great Financial Crisis had multiple negative growth quarters but started with a down and then up quarter. The 2020 COVID crisis had two consecutive negative quarters only because the very short recession overlapped the first and second quarters.

Sometimes quarterly economic patterns create short-term irregularities. The first quarter’s 1.6% decline in GDP had several. Personal consumption and investment remained robust. Declining federal spending from the end of pandemic-related support and weak exports, partly related to Russia’s invasion of Ukraine, caused the initial data release to show the economy shrunk in the first quarter. Those factors fail the test of the decline being spread across the economy. From a broader perspective, the vast majority of the economy remained strong. In fact, it was too strong, and the Federal Reserve was forced to embark on a program of rapid rate increases to tame inflationary pressures.

The weakness in the second quarter was broader than the first. Goods spending dropped 1.1%. Residential investment fell 3.7%, in line with our expectations that higher interest rates would pressure housing demand. Government spending also continued to decline as pandemic-related programs continued to wind down. Each of these areas experienced abnormal growth during the pandemic. People sought out goods to make social distancing less painful. The demand for housing rose rapidly as some people left big cities and others sought to expand their homes. Government programs supporting people displaced by the pandemic are no longer as necessary. Inventories also stopped increasing as rapidly as in previous quarters, pulling growth lower. What is bouncing back is services consumption, which increased 1.0% in the second quarter. Exports also bounced back from the temporary weakness in the first quarter.

While we don’t believe the U.S. has entered a recession, we do see the economy has slowed. Some of this pullback is necessary, as excess demand and lack of supply have caused unacceptable levels of inflation. Those inflationary pressures are quite broad. Wages rose 1.6% last quarter and are 5.7% higher than a year earlier. Core PCE inflation rose 0.6% last month. In order for inflation to move toward 2.0% per year, wage pressures will need to drop.

The recession argument wasn’t the only item that interested markets. The Fed also indicated it is seeing some signs of economic slowing. According to Fed Chair Jerome Powell, the recent rate hike has raised rates to a “moderately restrictive level” and the Fed will be more data dependent. Markets took this statement to mean the Fed is willing to slow interest rate increases if inflation starts moving lower.

Whether the U.S. ultimately enters a recession or not is still to be seen. Risks are higher than normal, but a recession, in our view, is far from certain. The Fed would like to avoid a recession, but previous comments suggest it would be OK with “softish landing” in which the economy entered a shallow recession and then rebounded without the inflationary pressure. The broader point is the Fed recognizes its policy has tightened materially and it will adjust its future outlook and not keep raising rates and creating a far worse economic slowdown.

The S&P 500’s 9.2% increase last month indicates the market is moving that way as well.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

BLOOMBERG U.S. AGGREGATE BOND

The Bloomberg US Agg Total Return Value Unhedged, also known as “Bloomberg U.S. Aggregate Bond Index” formerly known as the “Barclays Capital U.S. Aggregate Bond Index”, and prior to that, “Lehman Aggregate Bond Index,” is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

National Bureau of Economic Research. https://www.nber.org/research/business-cycle-dating

Bureau of Economic Analysis. 7/28/22. https://www.bea.gov/news/2022/gross-domestic-product-second-quarter-2022-advance-estimate

Bureau of Economic Analysis 6/29/22. https://www.bea.gov/news/2022/gross-domestic-product-third-estimate-gdp-industry-and-corporate-profits-revised-first

Bureau of Economic Analysis.7/29/22. https://www.bea.gov/news/2022/personal-income-and-outlays-june-2022

U.S. Department of Labor Statistics. 7/29/22. https://www.bls.gov/news.release/eci.nr0.htm

Federal Reserve. 07/27/22. https://www.federalreserve.gov/newsevents/pressreleases/monetary20220727a.htm

Federal Reserve. 07/27/22. https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20220727.pdf

Compliance Case #01445642